Superannuation fund trustees who receive compensation from financial institutions and insurance providers must consider how receipt of these payments may impact a member’s contribution caps.

A superannuation fund may have a right to seek compensation if it entered into a legal contract or agreement with a financial services provider or insurance provider, paid the fees or premiums from the fund’s assets, allocated the cost to the members, and:

- the financial service or advice was not provided

- the advice was deficient, or

- the insurance premiums for death or disability insurance cover were overcharged.

The compensation may include an amount reflecting a refund or reimbursement of adviser fees and/or an amount to compensate for lost earnings. It may also include an interest component.

If a superannuation fund receives such compensation, the fund’s trustee must be aware of possible superannuation, income tax and GST consequences for the fund.

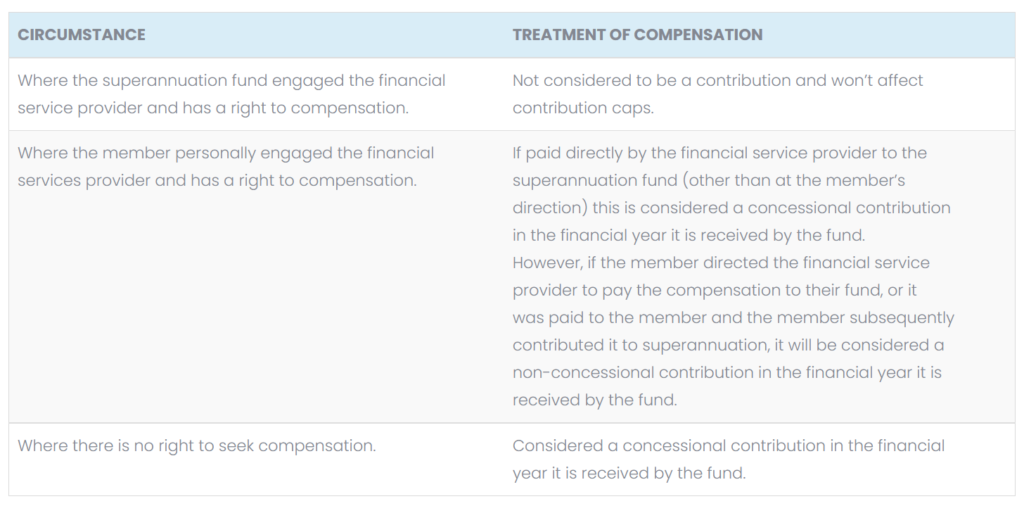

The implications for the fund and members

The ATO has released a superannuation contribution caps factsheet that explains how the receipt of compensation payments to a superannuation fund may impact contribution caps.

Whether compensation is a contribution will depend on the circumstances in which the compensation is received. The circumstances are summarised in the table below.

The following issues should also be considered by superannuation fund members who have received compensation payments:

- If the payment results in the member exceeding their concessional or non-concessional contribution cap, the member can apply to the ATO to request the Commissioner to exercise their discretion to disregard the excess contributions or reallocate them to another year.

- The ATO is unlikely to exercise its discretion if the compensation is paid to the member and the member contributes it to their superannuation fund, or the member directs the financial service provider to pay the compensation to their superannuation fund for their benefit. This is because making the contribution to superannuation is in the member’s control. If a compensation payment is a non-concessional contribution and causes the member to trigger the bring-forward rule, although the member may not exceed the cap in the first year, it could cause problems in the second or third years of the bring forward period. Where the member subsequently makes a contribution in the second or third years that results in the member exceeding their cap, the ATO has stated there would have to be special circumstances in relation to that contribution made in the later year for it to exercise its discretion.

- If the compensation payment is a concessional contribution, there may be Division 293 tax consequences if the member’s combined income and concessional contributions exceed the income threshold for the financial year they receive the contribution. From 1 July 2017, the Division 293 threshold is $250,000.

Further information can be found on the ATO website.

Please contact the TNR team if you have any queries relating to avoiding contribution issues with compensation payments.